Q2 2025 GVI Letter

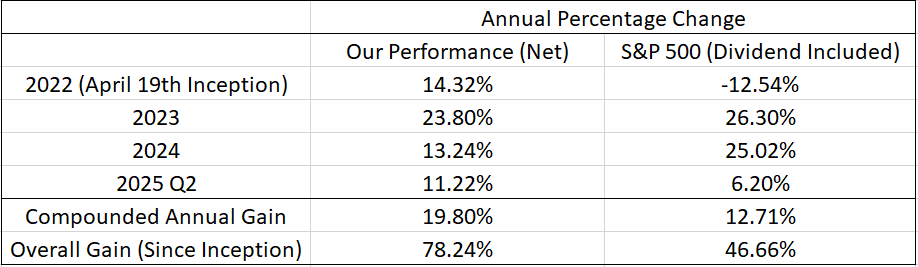

In the second quarter of 2025, we delivered a 5.75% positive return net of all fees, carries, and expenses, while S&P 500 returned 10.94% inclusive of dividend. Our main contributors include NetEase and TD Synnex, which we have discussed before. We massively added to TD Synnex after its puzzling panic sell-off after its last earnings call. It is now one of our top positions. Our main detractors include PDD, Kaspi, and Meituan, with the former two as core positions.

We believe PDD, Meituan, and Kaspi are managed by some of the best management teams we have ever come across, harness some of the best business models/ecosystems ever seen, and are trading at historically cheap multiples in a euphoric market setting daily all-time-highs. We are delighted to see Meituan’s continuous decline as we gradually nibble and build up our position. If it drops to below 100 HKD, we will gleefully make it one of our largest positions again, just like we did in early 2024 when rumor had it that Xing Wang’s own brother was shorting the stock (LOL). Therefore, although the US stock markets keep setting new all time highs, we remain confident in our portfolio holdings and believe they will deliver decent returns over the long-term.

TACO (Trump Always Chicken Out)

Q2 2025 feels like a drama. When the market sold off sharply after the Liberation Day, some talking heads and some of our peers turned bearish or lightened up their portfolio, and started to marvel at Buffett’s prescience in hoarding cash. We are bad macro-forecasters and our investors entrust their capital with us to pick stocks, not to guess where the markets will lead. We underwrite investments that we believe can deliver 12-15% of annual return with a reasonable degree of confidence in accordance with our long-term aspiration of delivering a net return in this neighborhood as delineated in our first investor letter. Further, as written in our 2025 Q1 investor letter, “The additional fiscal deficit caused by a recession could far outweigh any additional tax revenue collected from the tariffs” so we have always viewed the tariff threat as Trump’s negotiating tactics.

Therefore, as a reminder, we wrote the following paragraph to you on April 8th:

The United States is a system with checks and balances—Trump cannot act as he pleases. There's Congress, lobbying groups, Jewish influence, the Supreme Court, and a two-party system. Until last Thursday, despite Musk spending $20 million, the Republican Party had already lost the Wisconsin judicial election—and by a wide margin. Tariffs don’t recreate manufacturing. When swing states like Pennsylvania and Michigan realize this—and also feel the pressure of high inflation making life harder—they’ll respond accordingly. If this continues, that will show up in next year’s midterm elections.

Trump’s two biggest backers, Elon Musk and Bill Ackman, have both turned against him. Ackman is Jewish, and I’ve heard he’s been pressuring Trump via Jewish business circles. Is that pressure effective? I believe absolutely—because Trump’s caution around TikTok comes partly from the fact that one of TikTok’s largest shareholders is both one of his biggest campaign donors and a Jew.

Now, there are many signs of improvement. On the one hand, tariffs hawk Howard Ludnick did not hold a press conference today—whenever he appears, markets plummet, but today it was Scott Bessent who spoke instead. Bessent comes from a hedge-fund background and is closer to Wall Street, and he mentioned that the number of countries in active or potential negotiations has increased from 50 to 70. On the other hand, the EU has softened its stance, and countries like Japan, Vietnam, and Israel are responding cooperatively—these are all signs that things are moving positively. The United States is a country with checks and balances. It is not—and won’t imminently become—a dictatorship. I find it hard to imagine it heading completely down a dark path.

We adjusted our U.S. equity holdings at the start of this year, significantly reducing leverage across our portfolio (we replaced every company with net debt/EBITDA above 3×), cutting liabilities to ensure our holdings can weather the cycle. For each stock, we conducted extensive primary research and reviewed a large volume of secondary research. Although the market has pulled back recently, I haven’t seen any fundamental misjudgments so far. I will continue to closely monitor these companies.

That day marked the trough of this market cycle.

You can expect us to follow similar thought patterns on a going-forward basis. We do not have the ability of predicting what happens in the short-term, and our return should mostly be driven by our careful selection of businesses that conform to our investment standards.

The Trucking Industry

I started my career in the commodities industry. As time goes by, I start to focus a lot more on business model and quality. However, the habit of riding cycles dies hard, and I find the trucking industry going through a cycle that, in my view, is somewhat predictable, so please indulge me with allocating a portion of our portfolio in a well-managed trucking company trading at close to 1/2 of its liquidation value. In this letter, I hope to share my thoughts on the trucking industry, and my way of evaluating this cycle.

Based on data from the Bureau of Transportation Statistics below, you may observe a surge of rates during the pandemic. The limited supply, a surplus of savings partially aided by stimulus checks, and hoarding instincts led to the greatest bull market in trucking on record.

Since early to mid-2022, the cycle started to turn. Destocking took place, demand for goods eclipsed by demand for services as people move outdoors further exacerbated by inflation, trucking capacity added during the pandemic became a glut, resulting in the longest and worst trucking cycle since 1980’s.

Usually, an upcycle or downcycle lasts 12-18 months, but we are in the truckload downcycle for 36 months now. Mom-and-pop’s have made a lot of money along with receiving stimulus checks during the pandemic, and could afford to hang on longer than previous cycles, causing a prolonged supply glut; end market demand has been anemic as a result of high inventory levels, rampant inflation and lofty interest rates. Almost all publicly traded transportation companies we have talked to told us that this is the worst cycle they have gone through. It is worse than the Great Financial Crisis because during the GFC, interest rate was lowered and labor cost abated, so at least the cost side benefited; this current cycle, however, interest rate climbed, cost of leases and financing increased, labor cost along with social inflation ran rampant.

Nevertheless, we believe the cycle is likely to turn barring a severe industrial recession for the following reasons:

1). Through conversations with the executives of one of the largest commercial truck dealer, we have learned that mom-and-pop’s are wiped out in drives. The truck dealers keep a book consisted of named mid/large-sized fleet operators and small/mom-and-pop operators. The small/mom-and-pop operators do not have “names” and these nameless accounts have dropped by more than 50% cumulatively, over the last two years;

2). The point mentioned above is corroborated by a worsening credit conditions across the lenders (the charts last until mid-2024 and the credit conditions have further worsened since then).

Through scuttle-butt research we have found that the excess cash made through the pandemic boom and stimulus checks are draining out and mom-and-pop’s are finally collapsing under financial burdens.

3). The cycle has lasted long enough, such that we are starting to see more and more mid-sized fleet operators bailing as well. In April, we witnessed the spectacle of three players, C&C Freight Network, Best Logistics, and Best Choice Trucking filing for bankruptcies on the same day. Earlier in June, Dolche Transportation, Kentucky Logistics, and GD Transportation filed for bankruptcies as creditors claimed millions. The list goes on — it seems we are getting close to the capitulation phase of this cycle.

4). Coupled with supply exiting the industry, we are starting to see truckload rates pusillanimously inflecting in 2025.

From various sources, we have learned that rejection rates (the percentage of shipper’s requests that the operators are turning down — higher rejection rates are bullish) are rising, spot as well as contract rates are inching up, and supply & demand are rebalancing. One thing good about the cyclical industry is that by definition they go through cycles, and as supply continues to exit, the uptick is inevitable and we believe the upcycle is likely to come in 2H 25 or 1H 26.

And allow me to wish you a happy National Holiday with a horn of an eighteen-wheeler!

Great note, thanks for sharing. How do you track rejection rates ?