Q2 Investor Letter -- Two Worlds of Equities

The Opposite Treatment of US and Chinese Equities

Dear Readers:

In 2Q 23, we underperformed S&P 500 by quite a large margin. Net of all fees, carry, and expenses, we returned 1.8%, while S&P 500 returned 8.2% in the interim. YTD, our net return is 10.4%, vs. S&P 500’s 16.29%. This is disappointing, but by examining and reexamining our portfolio, I believe our holdings are undervalued, and should deliver satisfactory return in the future.

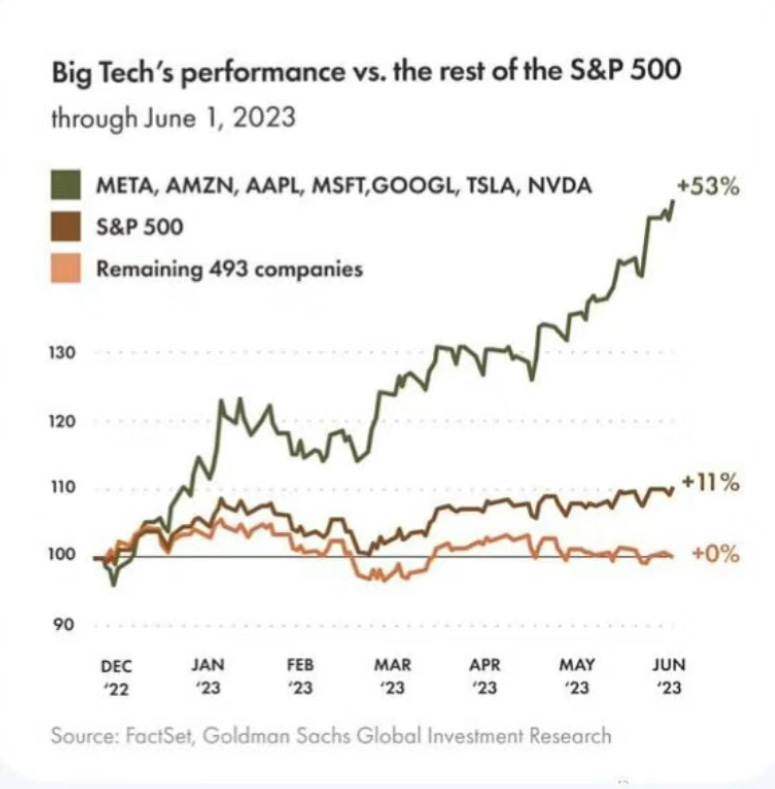

1H 2023 marks one of the most momentum-driven bull-runs of large caps, and attempting to beat the benchmark driven by these mega-caps has been difficult. Although some of the rally has to do with the bright prospects of generative AI, we believe the massive rally in stocks like Tesla is speculative (does signing a couple of charging station contracts warrant an addition of $250 billion market cap?). The rally of numerous businesses with potentially problematic business models (such as Carvana) further demonstrates the speculative nature of the market right now. We prefer to stay with businesses with competitive advantages, generating substantial free cashflow yield, and trade cheap with respect to their intrinsic value. We believe we are positioned to outperform.

Two Worlds of Equities

Under the recommendation of a friend who I greatly respect, Sean Stannard-Stockton at Ensemble Capital, I recently read Superforecasting. Two paragraphs on page 68 and page 69 echo with me profoundly. In assessing the difference between those who are great forecasters and those who aren’t, Philip Tetlock wrote:

One group tended to organize their thinking around Big Ideas, although they didn’t agree on which Big Ideas were true or false. Some were environmental doomsters (“We’re running out of everything”); others were cornucopian boomsters (“We can find cost-effective substitutes for everything”). Some were socialists (who favored state control of the commanding heights of the economy);, others were free-market fundamentalists (who wanted to minimize regulation). As ideologically diverse as they were, they were united by the fact that their thinking was so ideological. They sought to squeeze complex problems into the preferred cause-effect templates and treated what did not fit as irrelevant distractions. Allergic to wishy-washy answers, they kept pushing their analyses to the limit (and then some), using terms like “furthermore” and “moreover”, while piling up reasons why they were right and others wrong. As a result, they were unusually confident and likelier to declare things “impossible” or “certain”. Committed to their conclusions, they were reluctant to change their minds even when their predictions clearly failed. They would tell us, “just wait”.

The other group consisted of more pragmatic experts who drew on many analytical tools, with the choice of tool hinging on the particular problem they faced. These experts gathered as much information from as many resources as they could. When thinking, they often shifted mental gears, sprinkling their speech with transition markers such as “however”, “but”, “although”, and “on the other hand”. They talked about possibilities and probabilities, not certainties. And while no one likes to say “I was wrong”, these experts more readily admitted it and changed their minds.

Can you guess which group does better in forecasting?

(Super-forecasting, a book I’d recommend to anyone who tries to improve their forecasting skills whether to make better investment decisions or something else such as political forecasts.)

The first half of 2023 has two groups of people – actually, they might be the same group after all – those who believe China is utterly un-investable and sold off Hang Seng index the fourth year in a row (longest losing streak since its existence, YTD down 6.1%), and those who believe the magnificent seven (Apple, Google, Netflix, Tesla, Microsoft, Nvidia, and Meta) are flawless.

We decided to take the opposite side of them, snatching up dirt-cheap, high quality Chinese companies, gradually sold off our stake in Google, and starting to build short positions against Tesla, Netflix, and Apple.

Some of my conversations with my peers go like this:

Peer: “Seriously? You’re buying WH Group? What if there is a war between US and China, have you thought about that?”

Me: “Oh yeah, selling at 70% book, even if Smithfield gets confiscated by the US, their stake in Shuanghui alone justifies the current valuation. So why exactly are you holding Tesla at 65x 2023 PE if you think there is a war between US and China? You think the Shanghai Gigafactory’s gonna stay intact? You do know that most of Tesla’s operating profit came from that plant, right?”

Peer: “Seriously? You’re buying Conch Cement? Don’t you know that the real estate in China is collapsing, and consumption’s gonna be serious depressed?”

Me: “Sure enough, but Conch has a net cash position and the lowest cost in the industry, it’s a local monopoly that can expand as a natural consolidator of this industry; so when consumption in China is wiped out, you think that won’t affect Apple’s 20% sales in China? BTW, Conch is selling at 50% book (US peers sell at 2x), 2x normalized earnings adjusted for its large cash position, but Apple is issuing 5% debt to buy back its shares at a 3% earnings yield.” I did not even mention how Apple’s supply chain in China will be disrupted if there was ever a geopolitical conflict between China and the US.

The incongruence of logic is just everywhere.

Having learned how to fly in a living hell (namely the Hong Kong market), I have grown tired of “Grand Story Telling” – this war is imminent, and that collapse is coming right at you. Many of my peers simply do not look at individual businesses – instead of objectively assess risk adjusted returns based on fundamentals, they categorically cross-off the second largest economy in the world, believing in stories that may never realize. Like those China bears in 2001 when China was about to join the WTO, they simply tell you, “just wait, it will ultimately collapse”. Sure, in the long run, we’re all dead.

Therefore, I place my bets on lowly Conch and WH Group, betting they will substantially outperform the market darlings, 65xPE Tesla and $3 trillion market cap Apple in the foreseeable future. To complete the circle, we shorted Netflix to hedge against our longs in Warner Media Discovery, Disney, and Paramount, believing the other three platforms’ streaming user base has demonstrated the impossibility of a monopoly in this space, and 70x TTM FCF multiple certainly looks rich to us.

Briefly on these two largest holdings in our portfolio right now (we have gradually reduced our stake in PICC Property & Casualty, which we discussed in detail in our last letter, as it rallies):

Conch Cement (HK 00914):

1. Adjusted for a large net cash position, the stock is trading at 2X Price to Normalized Earnings. With a market cap of 100 bil RMB, 40 bil is net cash, and another 60 bil is long term equity investment -- you get the operations of one of the best cement companies on a global basis for free.

2. It has 40-60 years of limestone reserve, making sure it enjoys the lowest cost among all such players in China. It is not a victim; it is a survivor. It's expanding its aggregate business rapidly, and aggregate biz is better than cement. Think of a Vulcan Materials and Martin Marietta in the US (and observe their multiples!!)...

3. It has one of the best management teams, and it's a SOE, so no Alibaba types of private biz leadership risks.

4. It was giving away market share to sustain high cement price -- think of it as the Saudi Arabia of cement in China -- it's done doing that and it's crushing price right now to force smaller and/or leveraged players to go out of business -- it's working in spades. It's likely to be a natural consolidator at rock-bottom valuations across the industry, scooping up dirt-cheap competitors and realizing significant synergies down the road.

5. T-style strategy. This is the most unique part. T-style means it will produce upstream products that do not suffer from local economy characteristics associated with cement, ship the products down the Yangtze River, and then make the final product at local small mills downstream. Therefore, its radius of business operations is huge.

WH Group (HK 00288):

1. The entire sector of meat processing had too much capacity and the players in this industry are all cutting capacity, leading to a bottoming of this industry by the end of this year. This is the time to start to build a position – cyclical stocks turn earlier than the cycles themselves.

2. Despite much strongly 1Q 2023 performance than its US peers Tyson Foods, it is selling at a 20% discount (WH Group’s 1Q earnings was “only” cut in half, while Tyson Foods had a sizeable loss). Last year was tough, but the stock still managed to churn out a 12% FCF yield while significantly reducing its debt load at the parent level. By the end of this year, they will get rid of their debt at the parent level and start to buy back their stock (which they did in a large amount back in 2021 at 7.8 HKD/share and the stock is basically trading at half of that level).

3. They have already settled the 2013 Smithfield lawsuit and took a charge-off last year. The remaining lawsuits are unlikely to result in material losses, yet the market is still concerned with these lawsuits, giving the stock an unfair discount.

4. Gradually shrinking their fresh pork production which is the most volatile in connection with hog prices, leading to a more stable operating profit profile, possibly alleviating the cyclical discount.

5. Owner-operator Hongwei Wan succeeding Long Wan, and Lijun Guo managing the daily operations, interest alignment with small shareholders and friendly shareholder returns policies in the past with massive buybacks and a fat dividend yield at the current price.

We continue to hold M&T Bank (discussed in our 1Q letter) and Webster Financial, sold out our Western Alliance Preferred-A series at a nice profit, and built a position in Citizens Financial. We also added (or reestablished) positions in PDD, Beke, and Luckin Coffee, taking advantage of the ADR sell-off that happened (again) in 2Q 23.

No one can speak with certainty what will happen to the market, and what we do is simply to compare the risk adjusted returns across assets and companies and construct a portfolio that will hopefully be optimized. Let’s see what’s waiting for us in 2H 23!