When A Is Actually B -- Divergence of Expectations

One of The Most Profitable Ways to Make Excess Return

This is a brief note I wrote while riding an Amtrak train back to Boston from NYC. I’ve been thinking about this topic for quite a while and decided to jot down some notes for future reference. Many thanks to Mr. David Boyum at Landseer, a long-time friend and mentor, whose insights have stimulated my thoughts on this subject.

Diverging opinions create a market, and sometimes the consensus view can drive the fair value of an asset far from its intrinsic value. For instance, one stock, Supermicro, which we wrote about last year that we believe characterized the madness of the “AI Hype”, was thought to be a bellwether of AI, while in reality it’s just an hardware assembler operating in a competitive industry and its purportedly “proprietary” liquid-cooling strategy is no differentiation and easily replicable. This presented a profitable short opportunity, and those who blindly went long paid a hefty price. Another successful short we executed back in 2022 was Sunrun—the market viewed it as a renewable energy champion, while we saw it as a capital-intensive, highly leveraged leasing business that was bleeding cash.

Over the years, among the investment theses I’ve come across, two left a particularly strong impression on me.

The first one was written on United Rentals back in 2014. While the market believed United Rentals was a highly cyclical name susceptible to traumatic events such as the Great Financial Crisis of 08-09, the author(s) identified United Rentals as a compounder in a fragmented market with particularly attractive and valuable countercyclical cashflow that could be deployed for consolidation while the industry traded at depressed multiples. They also found that the stock was very cheap based on maintenance FCF—the seemingly high multiple was due to profitable capital investments for growth. The optical earning was depressed also due to United Rental’s aggressive depreciation schedule (and a correspondingly oversized capital gain upon disposal 3-4 years down the road). In other words, the market’s punishment of United Rentals (and related companies both public and private) for its apparent cyclicality was both exaggerated and ultimately worked in favor of its long-term consolidation mission.

(Source: Google)

Another beautiful thesis I have read was Rearden’s HCA long back in 2017.

(Source: Google)

The market feared the seemingly high leverage, along with potential political and reimbursement uncertainties associated with this hospital operator. Meanwhile, Rearden saw a low-cost operator protected by the umbrella of the majority of not-for-profit hospitals, which were operating at losses, and possessing a utility-like cash flow generation ability capable of managing high leverage while rapidly reducing its shares outstanding. She therefore wrote the following elegant words:

Utilities in the United States trade at an average of 22x earnings. (Alternatively, the S&P trades at 18x earnings, and HCA is growing faster than the average S&P 500 company and is arguably a higher quality business.) Should HCA—once the business is better understood and/or the scary healthcare headlines die down—trade at a similar multiple, its stock would be priced at $163 versus its current $86 price. That’s 90% upside, today. In a stock with which we see little downside risk.

When we wrote about Case New Holland (CNH) last year, we did not expect a heavy-weight like Mr. David Einhorn, a mentor and a friend who I send investment ideas to, will pitch the stock as well. Aside from this pleasant surprise, while the market focused on short-term negative sentiment among dealers and lackluster demand for agricultural equipment in general, we saw, first, a cyclical recovery, but more importantly, a justified long-term multiple re-rating driven by the rapid evolution of precision agriculture, supported by advancements in AI. We wrote:

One core thesis that leads to our investment in CNH is we believe CNH is the only player other than John Deere that has the capability of embracing the age of precision farming… … As CNH increases its precision farming sales as a percentage of its total sales, the subscription based, recurrent and predictable cash flow enabled by its digital services should naturally enjoy a much higher multiple than cyclical equipment sales.

We appreciate that Deere, Case, and Agco have the largest installed base of 2C hardware, which continuously sends back massive amounts of data. In turn, they can actively use these insights to develop new capabilities that significantly enhance farmers’ productivity. Not surprisingly, Deere is rolling out its 18-carame 9R tractors that autonomize tillage, while Case just started to deploy chatbots in its exclusive dealerships to improve their efficiency and better instant customer support. Many such industries that are already oligopolistic in nature will enjoy tremendously from this trend, since their tighter integration with infrastructure providers create silos that lock-in consumers, leading to the so called “oligopolistic platformization”. This year, we will devote more energy and attention span to identify these AI beneficiaries.

(Source: Digital Platforms in the Ag Sector)

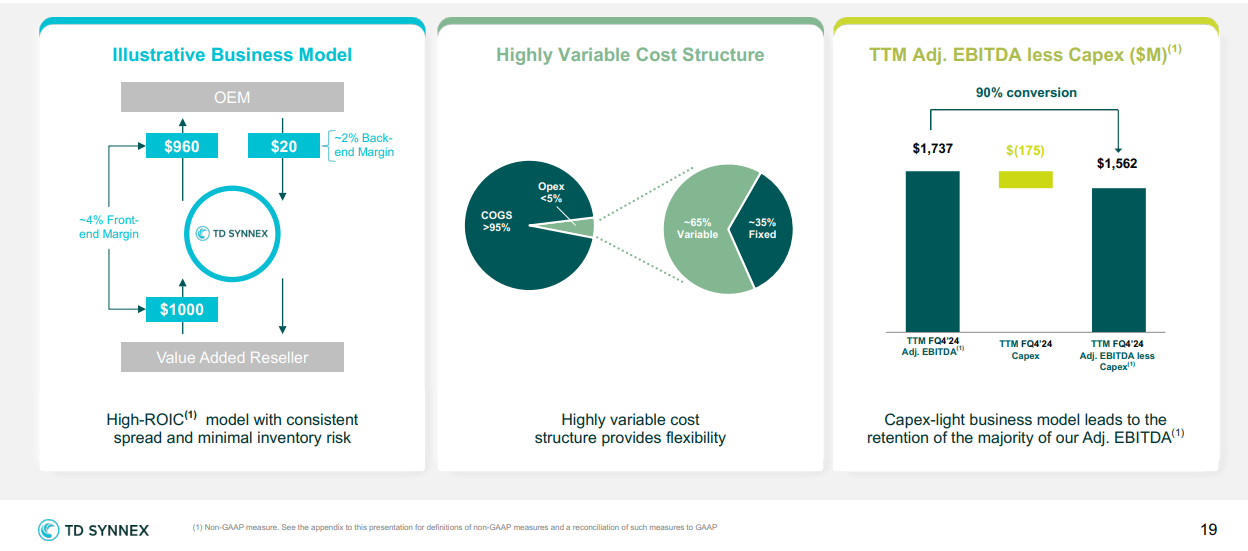

Another idea we wrote about (initially on Seeking Alpha and later on Snowball) was Ingram Micro. With full disclosure, we own both Ingram Micro and TD Synnex, and year-to-date, we are happy shareholders. Apart from a clearly progressing destocking cycle, we believe Ingram Micro and TD Synnex are in many ways similar to United Rentals and Ashtead. Many investors we’ve spoken to dislike these capital-intensive, low-margin businesses, while we see particularly attractive countercyclical cash flow that can be deployed in a value-accretive manner, along with a strong long-term tailwind from the advancement of AI. For investors willing to take a deeper dive, the distribution business is akin to a 'toll road' that takes a mostly 'fixed' cut for managing inventory and connecting with hundreds of thousands of downstream customers on behalf of the vendors. In addition, studies have found that these two-tier distribution models are empirically more profitable for everyone on the “food-chain” compared to direct-sale or one-tier distribution.

(Source: TD Synnex, 4Q 2024 Investor Presentation)

To sum up, my years of initially investing personal money and later serving as a portfolio manager have taught me that pure numerical analysis doesn’t create much excess value—as Steven Cohen commented, “everyone has a calculator.” Jim Chanos likes to say, “math is hard”, but look at where Kynikos is now… Over the years, I’ve met some investors who focus solely on numerical figures without truly understanding the underlying business models or the 'hidden stories' behind the optically observable numbers. To some degree, just perhaps, Seth Klarman suffered from this issue in the past decade as well. I do not discredit any investors and I respect everyone’s preference and style as long as they are logically self-consistent, but I believe the market is smarting up over time as a self-adaptive system (and probably even more so with the aid of LLM) and I just hope to be able to avoid value traps and continue to deliver nice returns for those who entrusted me with their capital. The important thing to keep in mind is to be able to sharply discern a mispricing when the market thinks A while in reality it’s actually B. As John T. Malone once commented to David Faber during a CNBC interview, “David, most of the money I have made in my life has been when people do not like what is going on.” Divergence of expectation (预期差) and a unique ability of picking the right side with deep insights separate an outstanding allocator from a mediocre one.

However, I hope to remain mindful of what I set out to accomplish—I do not intentionally try to be “different” by any means. As a friend of mine, Tim Liu at Meditation Capital, once commented, “I don’t like the term ‘variant perspective’—I just want to be right.” I couldn’t agree more. Empirically, more than a decade ago, the “consensus view” is Amazon, Visa, and Mastercard are wonderful buy-and-hold businesses, and Warren Buffett said his inability of investing in Amazon was due to “stupidity”. Yet, when the host asked Buffett why he didn’t buy now, he said, “Now it’s a $600 billion business.” Well, I am in absolutely no position to poke any fun here—I believe Jeff is one of the greatest entrepreneurs of our era, yet I was also too dumb to take a bite (or maybe I’m just afraid of heights…).

To sum up, I believe the best attitude toward intelligent investing might be: not to derive pleasure from either siding with or going against the market, but to objectively assess the business fundamentals where divergent perceptions could lead to mispriced odds that may, in turn, yield excess returns.

Chinese new year is days away, and I genuinely hope my readers a healthy and prosperous Snake Year ahead!