Q1 2025 GVI Letter

Navigating Tariff Uncertainties

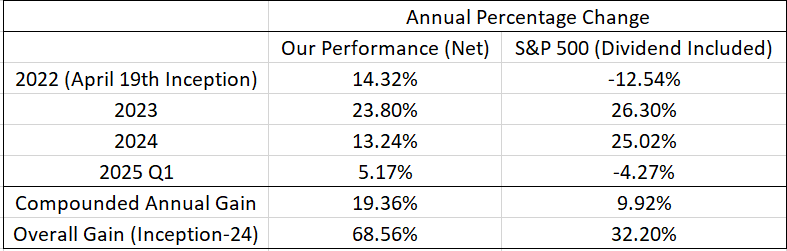

In the first quarter of 2025, we delivered a 5.28% positive return net of all fees, carries, and expenses, outpacing S&P 500’s return. Our main contributors include PDD and NetEase, which we extensively discussed in our Q3 2024’s investor letter, along with Tencent, which we will discuss in this letter. Our main detractors include almost all our US holdings (including TD Synnex and Ingram Micro, which we have discussed before) which we purchased to play the industrial cycle recovery discussed in our Q4 2024’s investor letter.

In another 18 days, I will be running my track record for 3 full years. I vividly recall early March 2022, when several of my colleagues' funds were liquidated as U.S.-listed Chinese ADRs were ruthlessly sold off, creating a downward spiral with almost no resistance. I was active in several WeChat groups, hyper-excited, encouraging everyone to put their life savings on the line to purchase those hated Chinese assets. I also remember my first "Great Miracle Day" on March 15, when seven top ministries simultaneously voiced their support for the Chinese economy, and my largest personal holding back then, PDD, surged more than 40% in a single day.

(This picture is for those of you who have watched the Greed of Man and can understand the humor).

I also remember that year's Berkshire Hathaway annual meeting. I had just returned to the U.S. from China and had no idea if there was even a chance that my investment strategy would survive. I watched the splendid dinner hosted by Giverny Capital at the Marriott Hotel (fortunately, I was invited to attend Giverny's dinner last year and will have the honor of talking to and learning from Mr. Rochon again this year), observing investment professionals commingling with each other, while feeling like a complete outsider. Walking around the scenic Chalco Hills Recreational Area, I felt a little lonely but also fortunate to have the company of hills and waters.

Three years have quietly slipped through my fingers. Hopefully, I have not let my investors down. At the very least, I cannot think of a better way to spend the last three precious years of my professional life—full of ups and downs, emotionally demanding (especially after the 20th Congress, during which I had an emotional breakdown, although, luckily, it did not impede my investment decisions), and absolutely thrilling in every imaginable way.

Industrial Cycle and Tariff War

The tariff war occupies the headlines these days, just as Russia, Ukraine, delisting, and China dominated the news when I first started managing third-party money in the U.S. Uncertainties are unavoidable, but they are often allies for rational investors capable of exploiting price dislocations created by excessive fear. Make no mistake, tariffs are very likely to be economically damaging, and due to their retaliatory nature, they are easier to initiate than to extinguish. According to the Federal Reserve Bank of Boston, a 25% tariff on all imports from Canada and Mexico, along with an additional 10% tariff on Chinese imports, could increase core PCE inflation by 0.5 to 0.8 percentage points. While tariffs may simply be a political weapon of the President, an escalation of the tariff war can easily spiral out of control. The additional fiscal deficit caused by a recession could far outweigh any additional tax revenue collected from the tariffs, so we hope rational minds will ultimately win.

Due to looming tariffs, our anticipated industrial recovery has been delayed. Companies we have spoken to, along with their suppliers and customers, are all waiting for the "tariff dust" to settle. It is difficult for companies to plan capital expenditures amidst significant uncertainties—businesses need a somewhat predictable macro-environment to project revenues and budget expenses. Although we have selected some industrial names with the best incentive structures, excellent operating histories, outstanding competitive prowess, secular growth in their end markets, and, importantly, clear signs of cyclical recoveries (for instance, inflecting inventory figures), the uncertainties created by tariffs have temporarily outweighed any progress of destocking in the short run; compounded by a general fear of an industrial recession, these stocks have been relentlessly sold off. We have been selling some of our appreciated positions in the Chinese market and opportunistically adding to these U.S. names. A delay in our thesis is, of course, not ideal, but we believe that, barring a severe global recession, these names are attractively priced at historically low cross-cycle multiples, and we will be rewarded as fundamentals and market sentiments shift.

Tencent as an AI Beneficiary

One of our largest holdings, along with PDD, was Tencent. I have not discussed Tencent extensively because there are numerous coverages and write-ups on this famed Chinese tech juggernaut. I hope to discuss Tencent briefly in this letter to illustrate how we approach investing by leveraging "variant perception" and "resonating cycles."

On December 22, 2023, while traveling with my wife in Las Vegas, the "Measures for the Management of Online Games (Draft for Solicitation of Comments)" appeared online. The gaming sector, having been repeatedly battered by regulatory pressures over the previous three years, utterly cratered. Tencent experienced large trading volumes and dropped double digits into the 270 HKD territory. As my wife and I watched some old movies in our five-star hotel room, I saw the news and Tencent's price action. I told my wife, "Please forgive me for several minutes; I need to place some trades"—this is the fat pitch I have been waiting for. This opportunity comprised three critical resonating cycles:

Market Sentiment Cycle: Tencent's gaming division had disappointed in 2023. Its archrival, NetEase, launched "Justice Online" and "Eggy Party" with tremendous success. Market sentiment toward Tencent was swinging to a negative extreme.

Industrial Cycle: In China, publishing a game requires a "game license number." The government had restricted granting licenses and referred to the gaming industry as "spiritual opium," preventing new game releases. During COVID-19 lockdowns, people played games to pass the time. As China reopened in early 2023, gaming time decreased just as the government relaxed license restrictions, leading to additional supply and diminished demand, resulting in difficult comparisons. In other words, Tencent was at the trough of an industrial cycle.

Liquidity Cycle: On December 22, liquidity was drained, funds were exiting Tencent en masse, and the stock plummeted. This is my favorite type of cycle, where opponents temporarily lose rationality and sell their positions regardless of their long-term outlook.

We quadrupled our position, that night.

As I was buying Tencent avariciously, I crossed my fingers and thanked Santa Claus – guess what, he really exists!

Like most Chinese securities, where volatility is almost part of the game, Tencent has not been a smooth ride. For months, Tencent was treading water. Sentiment was negative, and accusations of the inefficiency of its management team resonated among the investor community. The stock hadn't made a noticeable move even after its strong fiscal 2023 earnings report.

At the time of its fiscal 2023 earnings release, Tencent had a market capitalization of approximately 3 trillion HKD, with roughly one-third invested in securities such as PDD, which we have discussed previously. Netting out its various investments, it sported a 2 trillion HKD market cap, generated 200 billion HKD in free cash flow, and committed to a capital return of 100 billion HKD for fiscal 2024—a target it ultimately exceeded. The company had no debt and was managed by one of the finest entrepreneurs of all time. This constituted our margin of safety.

Tencent boasts the largest user base in China and possesses an unparalleled amount of user data—making it almost unimaginable that it wouldn't be a key beneficiary in the AI age. Indeed, one AI application after another emerged from Tencent, transforming what the market scarcely valued back in 2023 into our long-term call option.

The rest is history.

We feel very comfortable entrusting our capital to one of the greatest enterprises on a global basis that enjoys particularly strong economic moat and excellent network effect. Back in 2017, Pony Ma, the Chairman of Tencent said: “The first of our company’s core value is integrity. The managers we develop, and even our investors, share values that are highly consistent with ours. From the first day we accepted investment, I vowed never to let our investors down. Our company consolidates all its operations in one place; we do not use financial maneuvers to manipulate the company unpredictably. We do as we say. This commitment to contractual spirit is also one of our core values”. We adore this attitude, and as long as Tencent executes on its promises, this will be a very long-term holding of ours.

Insightful! Loved reading this.

Hello there,

Huge Respect for your work!

New here. No huge reader base Yet.

But the work has waited long to be spoken.

Its truths have roots older than this platform.

My Sub-stack Purpose

To seed, build, and nurture timeless, intangible human capitals — such as resilience, trust, truth, evolution, fulfilment, quality, peace, patience, discipline, relationships and conviction — in order to elevate human judgment, deepen relationships, and restore sacred trusteeship and stewardship of long-term firm value across generations.

A refreshing take on our business world and capitalism.

A reflection on why today’s capital architectures—PE, VC, Hedge funds, SPAC, Alt funds, Rollups—mostly fail to build and nuture what time can trust.

Built to Be Left.

A quiet anatomy of extraction, abandonment, and the collapse of stewardship.

"Principal-Agent Risk is not a flaw in the system.

It is the system’s operating principle”

Experience first. Return if it speaks to you.

- The Silent Treasury

https://tinyurl.com/48m97w5e